Featured Vendor

This section briefly explains IDC’s key observations resulting in a vendor’s position in the IDC MarketScape. While every vendor is evaluated against each of the criteria outlined in the Appendix, the description here provides a summary of strengths and challenges.

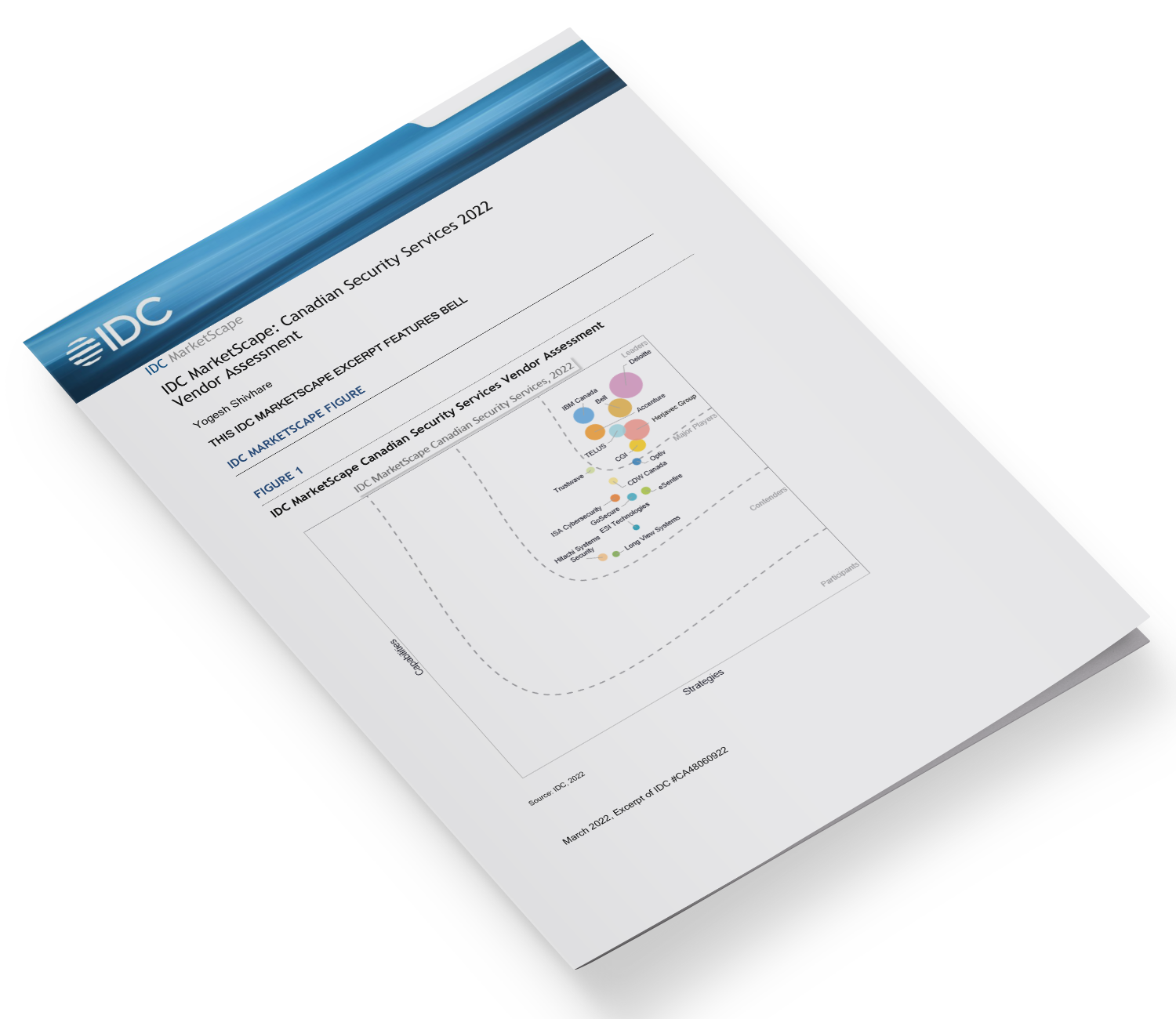

Bell

According to IDC analysis and buyer feedback, Bell is positioned in the Leaders category in this 2022 IDC MarketScape for Canadian security services vendor assessment.

Bell offers security services in Canada through its subsidiary, Bell Business Markets (BBM), and operates three commercial and one government SOC in Canada. The 700+ strong security staff is among the largest security teams in Canada and supports BBM’s customers as well as securing the Bell network. Bell has countrywide presence and can service midmarket and large customers across industry verticals.

Bell’s broad managed security services portfolio includes services such as network and content security, managed threat services (SOC services, MDR, and XDR), identity and access management services, cloud security, and IoT security. In 2021, Bell introduced BSURE (Bell Security Unified Response Environment), a Bell-operated and fully managed service that combines latest SIEM and security orchestration, automation, and response (SOAR) technology and Bell’s security expertise to deliver 24 x 7 monitoring, threat intelligence, alert triaging, and orchestrated and automated incident response to its clients. Bell’s MSS portfolio is complemented by an equally wide spectrum of professional security services including strategic consulting, assessment and testing services, and security design and implementation services that enable Bell to provide a one-stop shop for organizations looking to protect their entire ecosystem. Bell maps its security capabilities to clients’ security maturity and partners to transform it through five core security pillars — “simplify and solidify the core,” “SOC optimization,” “enhanced MDR services,” “addressing the velocity of cloud,” and “enabling convergence at the IoT/5G edge.” In addition to these core security service offerings, Bell also offers connectivity and networking services such as SD WAN, managed wireless, and DNS and VNS with embedded security.

Bell is making significant investments in proprietary AI/ML use cases, cloud security, IoT security, and automation within its technology, business support, and customer engagement processes. This enables Bell to add new services, enhance its existing portfolio, and improve customer experience.

Strengths

Bell customers cite the company’s scalability and maturity to deliver large and complex projects as its strength. Bell’s extensive partnerships with security technology providers and cloud providers enable the company to offer integrated, end-to-end secured solutions to its clients.

Challenges

Large organizations do bring the benefits of scale and maturity; however, Bell must demonstrate that it is nimble to customers to prove that it can quickly adapt to the changing dynamics of security projects.

Consider Bell When

Organizations looking to unify security management across the enterprise, including connectivity, security, cloud, mobility, and IoT, should consider Bell.

Learn more about how Bell can help you with your security needs.