Featured Vendor

This section briefly explains IDC’s key observations resulting in a vendor’s position in the IDC MarketScape. While every vendor is evaluated against each of the criteria outlined in the Appendix, the description here provides a summary of each vendor’s strengths and challenges.

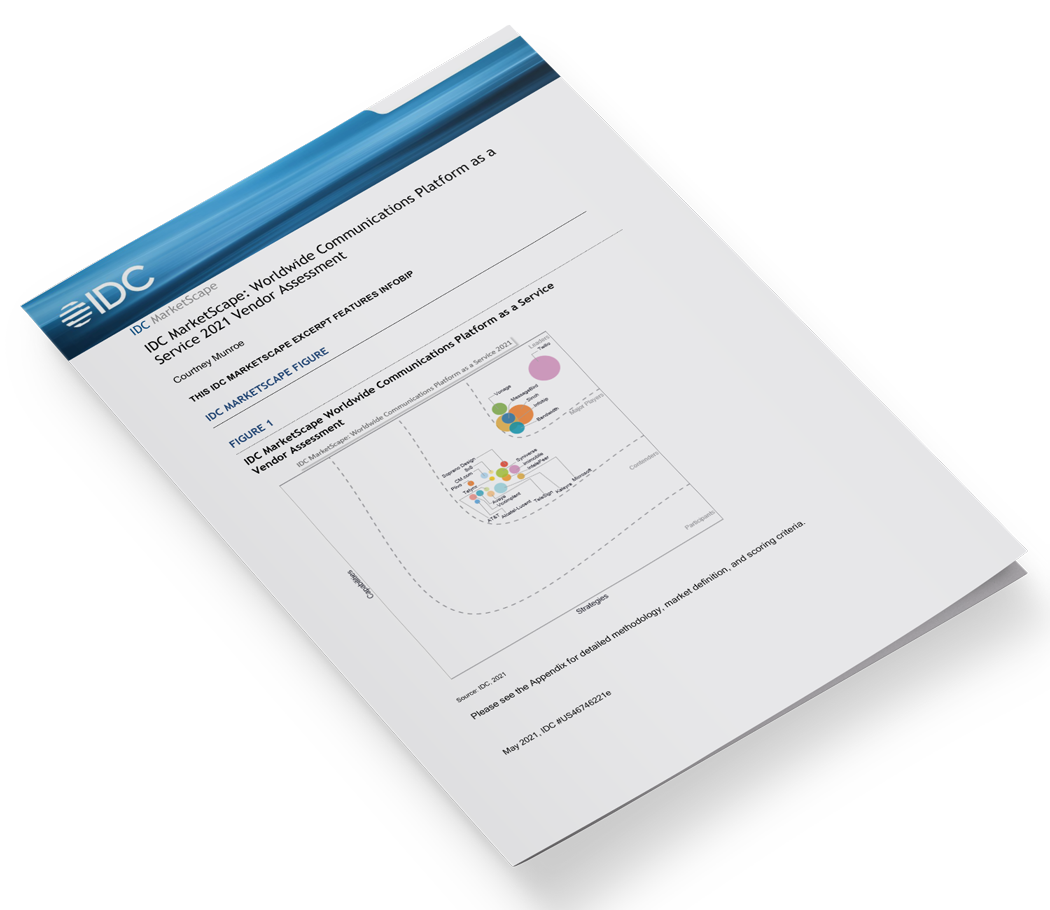

Infobip

Infobip is positioned in the Leaders category in the 2021 IDC MarketScape for the worldwide CPaaS market.

Infobip is one of the largest and highly diverse global CPaaS providers. The company offers a wide range of APIs, interconnection services for mobile network operators, and customer engagement SaaS for enterprises in a wide range of industries. Over the past decade, Infobip has evolved from a focus on messaging services to mobile operators to a full stack CPaaS offering customer engagement and solutions and communications APIs. Its November 2020 acquisition of OpenMarket adds a much-needed boost to its presence in North America.

Strengths

Infobip’s key differentiator is its broad portfolio, global scale, and footprint. The platform is segmented into three main segments. Infobip offers a full suite of APIs, including voice, SMS, RCS, email, chat apps, and OTT messaging services. Its solutions portfolio includes conversations, contact center integration, and customer data integration. Its connectivity platform offers numbers, identity services to banks, and IoT connectivity. The company has a global presence with offices in over 60 countries on five continents and completes 14 billion transactions per month to over 190 countries. The company has a great reputation for reliability and solid round the clock support.

Challenges

Infobip can be characterized as one of the most widely used CPaaS you never heard about. The company’s global platform is interconnected with over 600 mobile operators that also white label several of its solutions. As CPaaS becomes more competitive, Infobip will need to improve its visibility in key markets beyond its European home base. Its OpenMarket acquisition will provide a major boost.

Consider Infobip When

Global scale and local regional support is a key requirement for your company. The company also provides a broad portfolio for enterprises and offers carrier-grade service that is a crucial foundation for many network operators to deliver global messaging services.

Find out more about Infobip here