Featured Vendor

This section explains IDC’s key observations resulting in a vendor’s position in the IDC MarketScape. While every vendor is evaluated against each of the criteria outlined in the Appendix, the description here provides a summary of each vendor’s strengths and challenges.

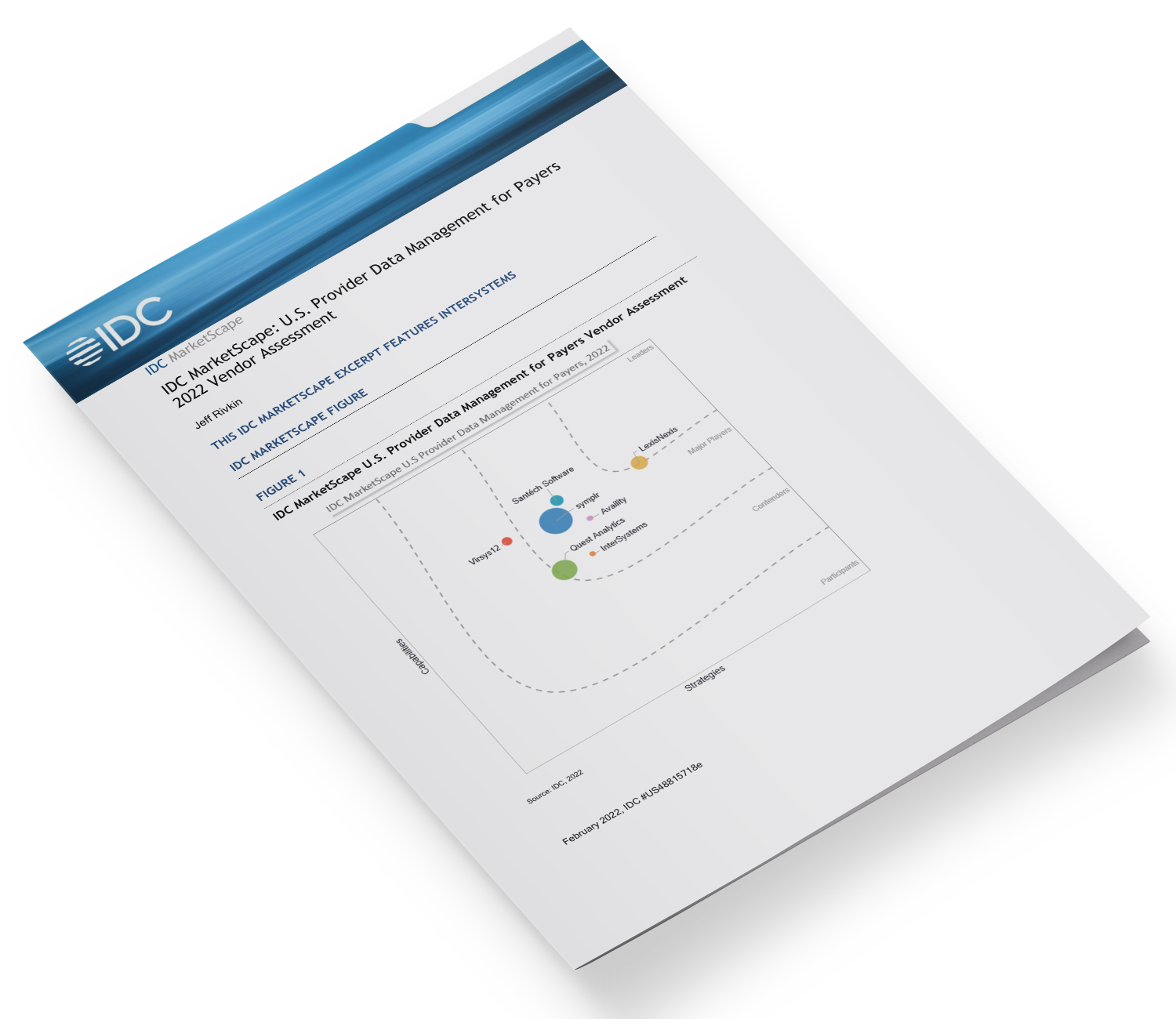

IDC’s assessment includes seven vendors: Availity, InterSystems, LexisNexis Risk Solutions, Quest Analytics, Santéch Software, symplr, and Virsys12. Other vendors did not meet the inclusion criteria and they will be highlighted in an upcoming document featuring the vendors to watch for provider data management in 2022. Those vendors are NTT DATA, Ribbon Health, Salesforce, SKYGEN, and Simplify Healthcare.

InterSystems

According to IDC analysis and buyer perception, InterSystems is positioned in the Major Players category in this IDC MarketScape for provider data management for payers software in the U.S. market for 2022.

Product: HealthShare Provider Directory

InterSystems, a global player in information technology platforms for health, finance, and government applications, founded in 1978, and serving payers since 2005, is privately held and offers HealthShare as one of its product suites. InterSystems has been providing interoperability solutions for decades internationally for many industries. Its ability to atomize, aggregate, deduplicate, and normalize data clearly is and has been its focus.

HealthShare is a suite of connected health solutions, and Provider Directory is a standalone purchasable unit that has been in the suite since 2019. It alternatively can be used within HealthShare as a directory FHIR resource and to maintain a provider registry for notifications. For example, a HealthShare buyer could purchase the following individual products:

- HealthShare Unified Care Record with FHIR Gateway. Provides an aggregated, deduplicated, and harmonized view of a member’s care record

- HealthShare Health Insight. An analytics product, dependent upon HealthShare Unified Care Record, used for dashboards, data quality, as well as to aggregate and clean data to use with other analytics solutions

- HealthShare Patient Index. An enterprise master patient index (EMPI) solution that provides an automated and easily integrated solution for creating a “single source of truth” for patient identity and demographic information

- HealthShare CMS Solution Pack. A turnkey solution for CMS-9115-F Interoperability and Patient Access Final Rule

- HealthShare Personal Community. A member self-management and engagement solution dependent on Unified Care Record

- HealthShare Care Community. A solution for care givers, patients, and their families to improve communication, care transitions, and care coordination outside of the hospital setting

- InterSystems IRIS for Health. An innovation and development platform to develop applications internally and used as the base of the HealthShare and other suites

- HealthShare Provider Directory. A master data management (MDM) solution for provider data to support member attribution and alerting (optional, standalone)

HealthShare Provider Directory, introduced in 2019-2020, on premises or hosted, focuses on master data management. Its data model and its understanding of the interoperability between payers and providers is its strength. Its core solution centers on the following key functionalities: data ingestion; data preparation and cleaning/normalizing; parsing data into the data model; matching and linking based on customizable rules; operational data management, such as validating matches, running queries, and updating records; and sharing and exporting data in multiple formats including FHIR.

HealthShare Provider Directory also offers a provider identity matching engine that combines deterministic matching, probabilistic algorithms, and defined rules to create, manage, and maintain the complex relationships that define the healthcare landscape, such as organization hierarchies, network participation, and multiple practice locations for provider information. Its Provider Directory is built on the HealthShare platform that includes interoperability tools combined with a push service that maintains a directory FHIR repository and can supply master data management records’ updates to downstream systems with accurate, up-to-date, reliable information.

InterSystems offers an on-premises or cloud solution in a “per provider” pricing model.

For data ingestion, HealthShare uses a suite of tools to enable interoperability among and onboarding of healthcare systems. Key tools in the ingestion process are:

- Out-of-the-box adapters for working with healthcare standard formats, custom formats, and standard protocols with prebuilt mappings for common healthcare standards

- Intuitive visual data mapping and process orchestration tools

HealthShare processes inbound records as data events, allowing rules-based action triggers based on transactions flowing through the system. As data is ingested, it is also made available in a relational data model for operational reporting and analysis.

Regarding curation of data, HealthShare ensures the consistency of data in several ways:

- Message validation

- Matching records across data sources, which can match deterministically or probabilistically using matching algorithms (Matching rules and linkage models can be customized, and customers can tune weightings and thresholds.)

- Normalizing various formats into a single comprehensive data model and applying code system mappings to normalize codes to a chosen target code system

- Role-based access for data stewards who maintain the directory

Strengths

InterSystems is extremely experienced in health data and its management. Its preexisting adapters for mapping standard data formats that facilitate data onboard show its commitment to (international) standards, and it serves on standards bodies (DaVinci, DEQM, Carin, INTEROPen, FHIR, HL7, and IHE). Tangentially, it is notable that EPIC relies on InterSystems development technology for its EHR software and expertise in infusing data into the EHR workflow. It also serves as the engine for 12 state health information exchanges (HIE) and the eHealth Exchange. The eHealth Exchange is active in all 50 states, is the oldest and largest national health information network in the United States, and is the principal network that connects federal agencies and nonfederal organizations, including over 75% of U.S. hospitals and tens of thousands of clinics, to share patient records to better treat patients and coordinate care. This shows its expertise in scalable bidirectional data exchange and an understanding of standards, certifications, and state regulation.

Challenges

InterSystems does not support campaigns for recruiting, onboarding, search (although it has REST and FHIR API implementation guides), outreach, attestation, self-service, CAQH/SAM/PECOS/LexisNexis validations, network adequacy, provider ratings, or sanctions, but these are on its road map and the data model is extensible.

InterSystems’ focus is on cleansing and identity so that the company’s core HealthShare applications and external interfaces have good provider data to execute with, including adherence to DaVinci methodology. InterSystems has an expertise in claims, enrollment, clinical, and SDoH data integration. Its slant on its provider data focus shows that lineage.

Consider InterSystems When

Consider InterSystems when you want a very health-oriented, international, experienced, data-centric, professional software vendor that understands the importance of clean data, governance, and the role of provider data integration in the interoperable health ecosystem. Its experience in HIE, payers, providers, finance, and government show its dedication to data engines providing accurate data as the commerce for better health.