IDC Opinion

It is cliche at this point to say that the COVID-19 pandemic radically changed the way that we work. From location to time, from blurring the boundaries between work and life to profound restructuring of the labor market, the past two years ushered in changes many thought were decades away. This, perforce, forced a change to all software markets supporting remote work, asynchronous work, and workforce automation. To meet this challenge, organizations purchased a wide variety of solutions including virtual client computing (VCC).

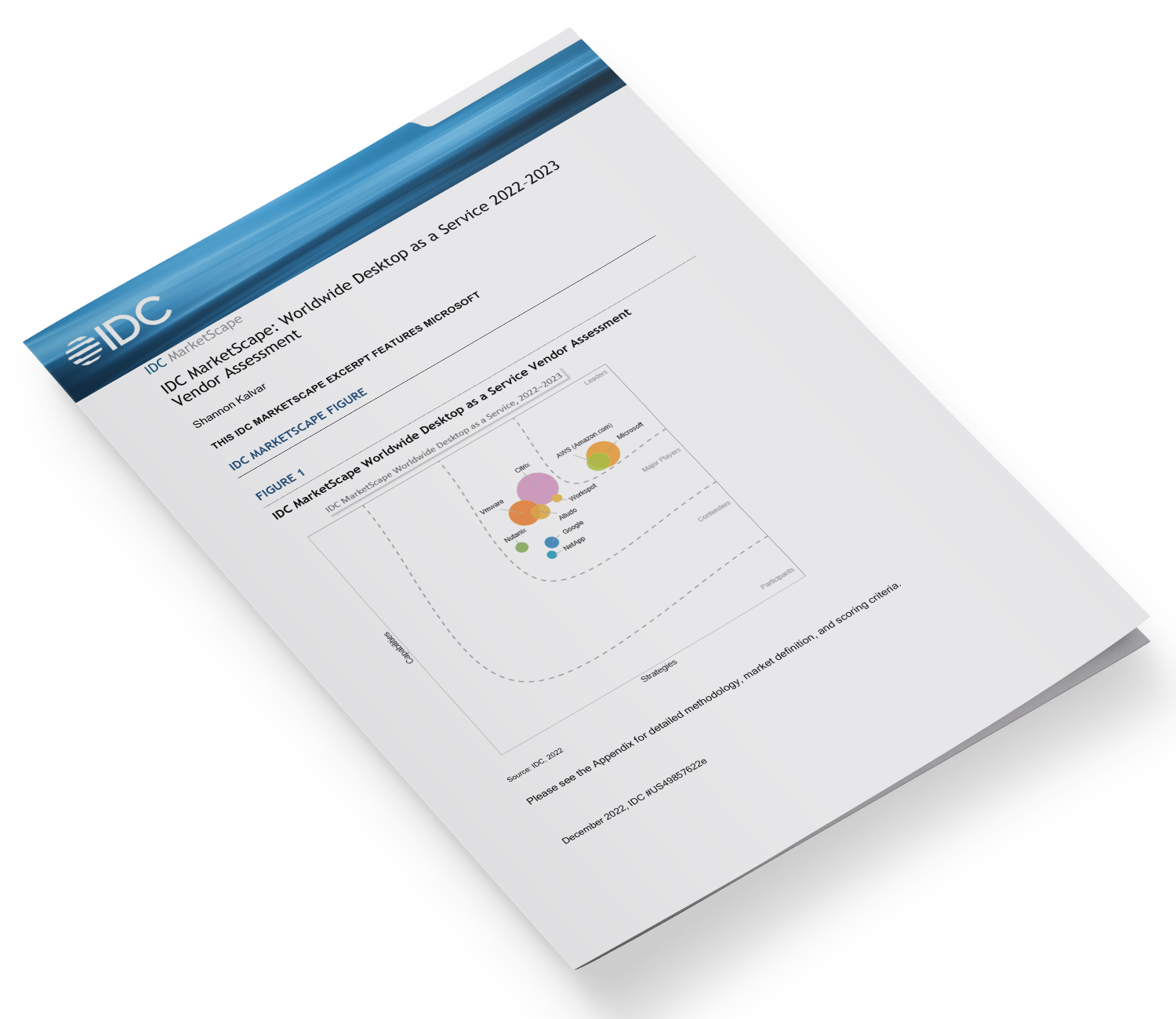

Desktop as a service (DaaS) is one modality of the virtual client computing market and is encompassed in the larger VCC IDC MarketScape (see IDC MarketScape: Worldwide Virtual Client Computing 2022–2023 Vendor Assessment, IDC #US49857422, November 2022) published contemporaneously with this one. It is also, however, a unique approach to application and desktop virtualization, combining software, prescriptive infrastructure as a service (IaaS), and some degree of professional services, many of which are automated or included within the design.

DaaS emerged as a potential service offering alongside more general cloud computing as was initially focused on including cloud infrastructure resources into existing virtualization solutions. However, it quickly became apparent that more was needed. In particular, customers pushed for defined specialized IaaS configurations, often including graphics acceleration, for specific use cases. They also began to push for opinionated architectures, monitoring solutions, and professional operations and management solutions.

This later need was originally met (and still is in some cases) by professional systems integrators and managed service providers (managed SPs). However, the resource constraints which appear as early as 2017 and became acute in 2020 pushed providers forcefully into offering more and more automation and inbuilt observability, sometimes isolated from the larger cloud environment, sometimes focused on endpoint management, and sometimes integrated into the larger ecosystem.

This larger ecosystem concern again forced divergence on the “DaaS” market, leading to a wide variance between solutions all offered under the same label. Customer interviews and survey results both point toward this being a large area of confusion, one which will be addressed in future research projects.

Finally, DaaS’ genesis as a “cloud first” technology means DaaS has been particularly susceptible to the trend revealed in IDC’s June 2022 Future Enterprise Resiliency and Spending Survey, Wave 5, where enterprises look first to their primary public cloud providers as their primary strategic technology provider, followed by their primary hardware vendors. This has forced the public cloud providers to step up, offering unique DaaS solutions that meet the strategic requirements of their largest customers.