Featured Vendor

Toshiba

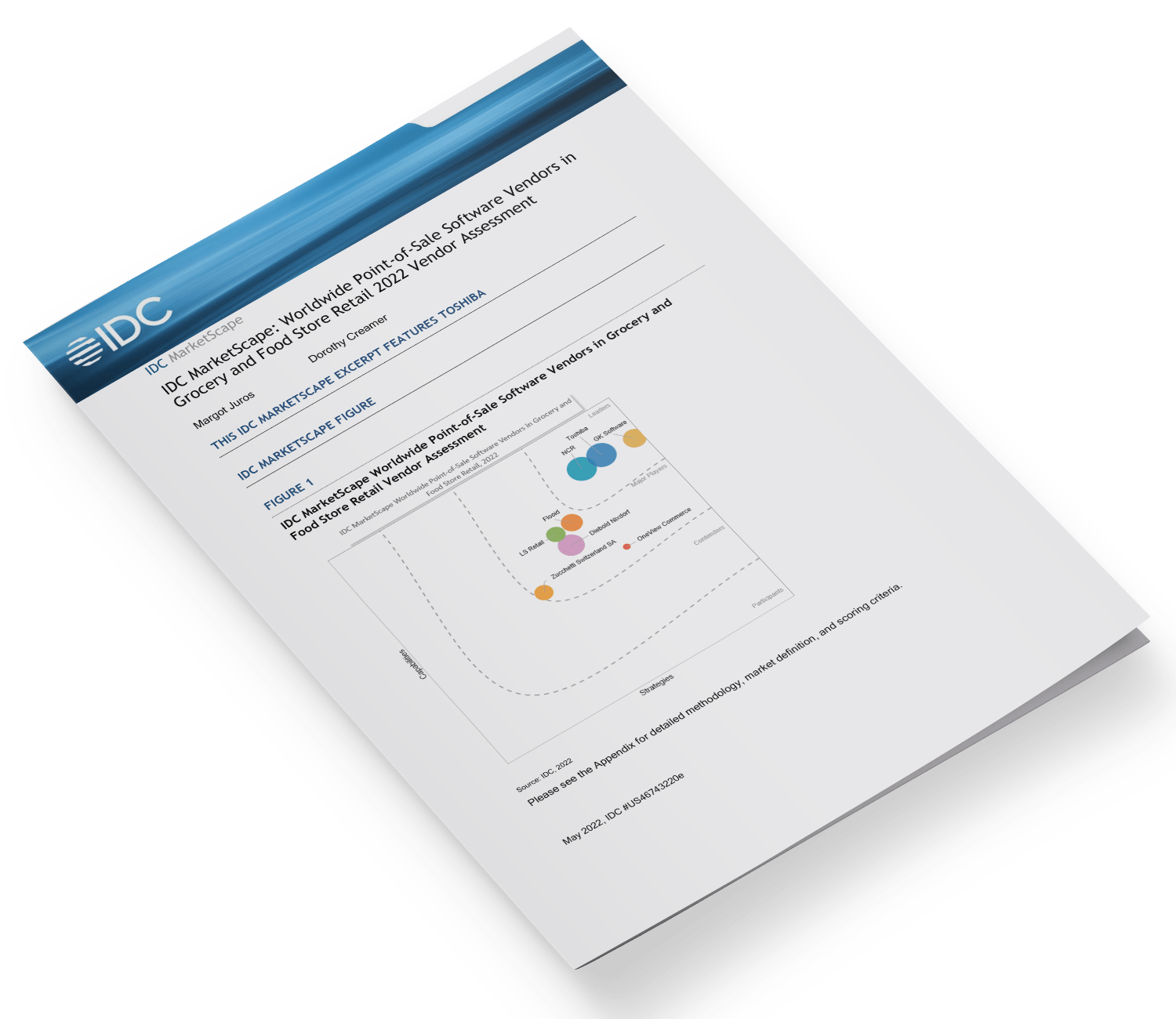

Toshiba is positioned in the Leaders category in this 2022 IDC MarketScape for worldwide point-of-sale software vendors in grocery and food store retail.

Toshiba Global Commerce Solutions, a wholly owned subsidiary of Toshiba TEC, is based in Durham, North Carolina, with nearly 3,000 employees, more than 3.5 million POS systems deployed, 1 million lanes of POS software installed, and in use by 500+ retailers globally. Toshiba TEC is 50.02% owned by Toshiba Corp., and the two companies are separately publicly traded companies. Toshiba was formed as a result of Toshiba TEC’s acquisition of IBM’s Retail Store Solutions (RSS) business and point-of-sale solutions in August 2012 and is now one of two retail organizations within Toshiba TEC. The Retail Solutions Business Group (RSBG) serves the domestic Japan retail market, while Toshiba Global Commerce Solutions is the primary organization that serves the rest of the world outside of Japan.

With 50 years of experience in the POS market and retail overall, Toshiba has firmly established itself in the upper echelon of POS software systems installed. Since 2017, Toshiba has pivoted to a platform-centric focus, first with the introduction of its TCx Elevate in 2017 and currently with the all new ELERA open, modular commerce platform, launched in 2020.

Toshiba’s POS solutions are a component of the company’s broader, cloud and digital-native, ELERA end-to-end modular, unified commerce platform. The platform is designed to alleviate the problem of traditional monolithic application architectures in which store, mobile, and ecommerce apps are developed independently, leading to data silos and fragmented experiences for customers.

The ELERA platform embraces modern technologies to take unified commerce to the next level including microservices, retail store digital twin, IoT, edge, data analytics/visualization, and computer vision.

ELERA’s microservices architecture, with more than 50 microservices and over 550 APIs, utilizing API first principles, allows for seamless interaction between applications, devices, and services across channels — enabling a common, consistent consumer experience across all channels, whether head or headless. ELERA also simplifies management for retailers providing a comprehensive view of the entire retail infrastructure and one source of customer data (one source of truth).

Modules built on the ELERA commerce platform currently include POS, self-service, ecommerce, loyalty and promotions, frictionless store, shelf inventory/queue management, item recognition, and commerce analytics. Payments and experience are the other two main modules of the platform, including areas such as payment analytics, alternative payments, and customer analytics. Retailers can take a “mix and match” approach, selecting the modular components best suited for their operations, as well as utilize their own or third-party applications.

Toshiba has infused the platform with a range of modern technologies such as IoT and edge control that allow retailers to enable a range of use cases built using computer vision and AI/ML and edge devices such as item recognition, loss prevention or shelf monitoring, unified data lake, and data visualization/analytics. ELERA also includes self-enablement tools that allow retailers to develop, experiment, trial, and scale their own unified solutions, enabling them to respond quickly to shoppers’ changing preferences and needs.

Toshiba traditionally focuses on the high-volume retail segments where speed is essential, including grocery, mass merchandise, and drugstore, targeting tier 1 retailers. It serves tier 2-4 customers through an extensive partner program and network supporting other software applications for hundreds of tier 2–4 retailers. It is currently engaging partners to extend ELERA to these customers.

Geographically, Toshiba has a global focus with clients around the world and provides end-to-end support for its customers. Its biggest regions are North America and Europe. With a focus on cohesive customer experiences across channels and retailer control and empowerment, Toshiba has steadily introduced a stream of new features and enhancements for ELERA over the past two years, including produce recognition, self-service kiosks, enhanced loyalty and promotions, and mobile applications. Toshiba’s road map moving forward includes furthering the company’s vision for building new and enhancing existing platform solutions such as frictionless store, shelf monitoring, consumer mobile applications, and new payments abilities.

Strengths

- Toshiba Global Commerce Solutions stands out with its global presence, large installed base of POS systems, strong omni-channel vision and road map, long record of innovation, and demonstrated ability to meet evolving business needs, making Toshiba a formidable competitor.

- Toshiba’s ELERA platform stands apart from many competitors with its embrace of modern technologies throughout the platform to take unified commerce to the next level including IoT, edge, data analytics/visualization, and computer vision. Its microservices architecture allows seamless interaction of applications of the retailer’s choice across channels while maintaining a common user experience across the platform (head or headless).

- Toshiba offers retailers great flexibility for payments from the platform, acting as a connector between POS and payment gateways. Retailers can use an existing payment gateway or Toshiba gateway thereby eliminating the need for third-party vendors in the middle.

Challenges

- Toshiba is currently rolling out ELERA to its tier 2 and tier 3 customers through its extensive partner network, and the company will need to learn more about how smaller retailers can utilize ELERA. In addition, pricing structures will need to be developed to align with the needs of these potential customers as they evolve to the cloud. Today, Toshiba does have an extensive channel program and network supporting other software applications for tier 2–4 retailers that it would need to engage and extend for ELERA.

- While Toshiba’s open platform is well designed to meet the needs of omni-channel retailers at any scale with enhanced next-gen technologies, it may face the challenge of interconnecting point solutions from smaller, extremely focused competitors in areas such as AI. Retailers will look to Toshiba to incorporate these solutions into their retail environment. The company is building an ELERA ecosystem that could potentially turn this challenge into a competitive advantage by enabling retailers to plug all devices and applications into ELERA and scale them across their entire retail IT infrastructure.